There is a large number of lenders around. For the upside, since the a prospective homeowner you are blessed to the gift of preference. For the downside, you to definitely possibilities can be difficult. How do you narrow down your options? Which are the situations you must know?

Basic some thing earliest, do your homework. There are a lot of key facts and you can answers that you is also determine oneself prior to actually meeting with a potential mortgage lender.

Create a preliminary search of all of the lenders in your area. After you have a substantial checklist, get breaking on your own research. Physically, I suggest and make good spreadsheet (or something of for example) where you can list the important points for each and every bank. Begin by for each lender’s webpages, however, make sure you grow with other websites to see what other people say about this style of financial.

Credible sites like the Bbb are a great ways establish the fresh new lender’s credibility just in case they are inside a great standing. If they’re detailed and also reviews that are positive, they’re probably an established alternatives. While doing so, every financial and you will mortgage banker are supplied a different sort of NLMS amount. Through the NMLS User Availableness, you could confirm that a friends otherwise personal is actually authorized so you’re able to do business on your county. Very which is a good spot to check, as well. After you have blocked out whom you do not want, it’s time to place a meeting otherwise label into the lenders who possess generated new clipped up to now. To arrange to suit your cash advance near me conference, You will find come up with particular important questions to inquire of. Tip: Via your dialogue, pay attention to the manner in which the potential financial responses the questions you have. If you believe like these are typically apprehensive to present suggestions or he is intentionally providing you with vague, cutting-edge solutions, you can even think marks you to financial away from your own record.

1. Just what are the offered mortgage apps?

Of many lenders keeps several mortgage alternatives. Make sure that it let you know all of the possibilities, not simply the ones they suggest. You have the to consider all of your options.

dos. Exactly what are your own charge?

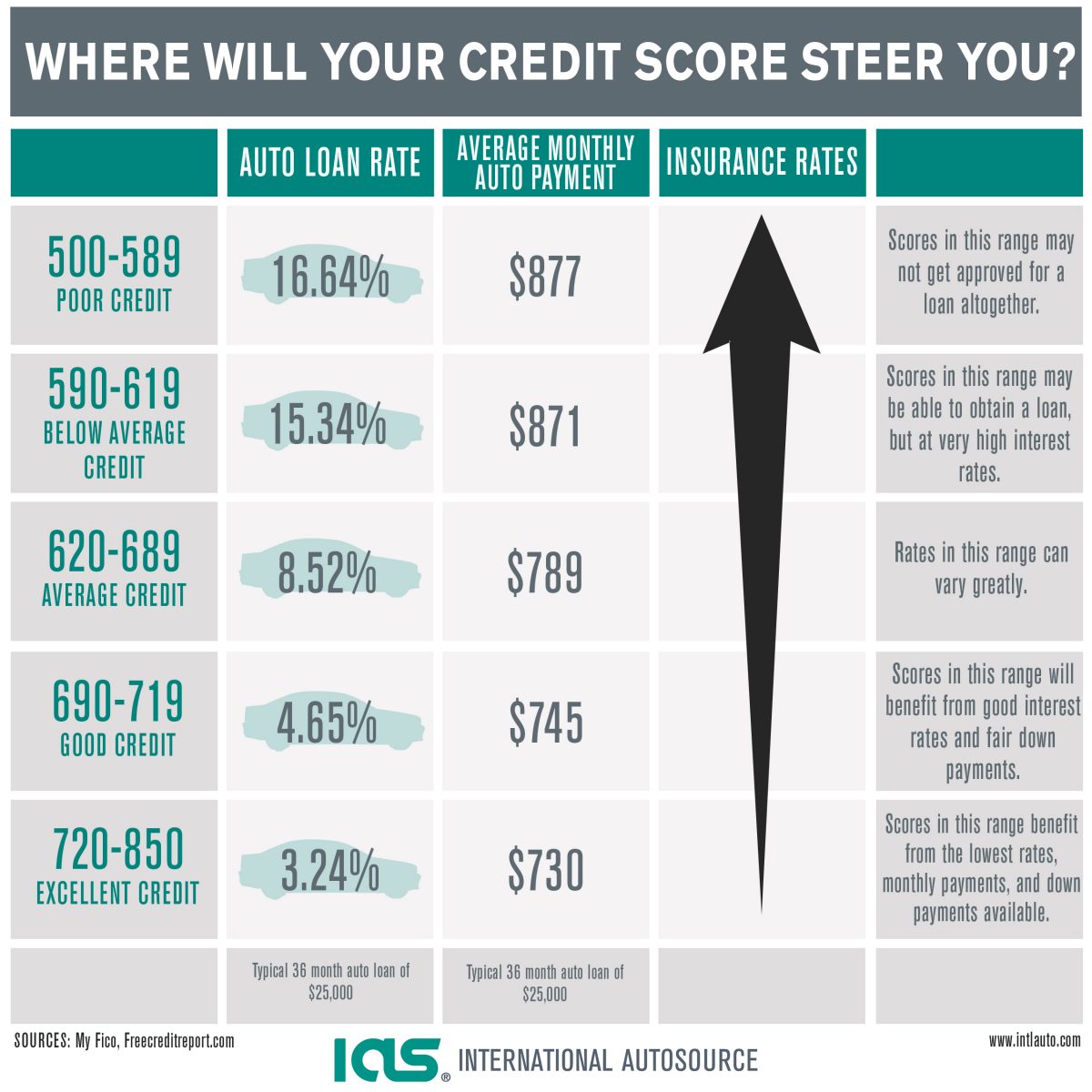

This really is a good biggie to many homeowners. You’ll find important charge in the business, right after which you will find costs one vary for every lender. Make sure to separate the 2, and inquire the lending company supply as much outline to for every payment. Such, they need to choose which can be apartment-price charge, and you can that are charges calculated because a portion of some other profile.

Seriously consider both definition and you may schedule of each and every commission. Its preferred observe an identical percentage named different things each lender.

Additionally, a lender may waive a particular payment, in real world it is simply deferred to help you after within closure. Eg, certain can get feature which they waive upfront app charges, but charges a hefty commitment percentage on closing.

step three. Would you provide upfront underwriting?

Initial underwriting is another term you to passes more labels each lender. In short, upfront underwriting is where your financial can also be comment your credit history as well as your earnings documents, before also with a home target. With this particular process, you will be conditionally approved even before you begin family google search. Therefore you will understand what you are able really manage first household query. Alternatively, a loan provider who merely offers pre-certification typically does not verify money advice up to once you’ve an effective assets address and you can ratified bargain. It ount that significantly change later on later on – perhaps once you’ve currently lay their heart for the property that’s now away from the loan funds. As you can plainly see,initial underwriting has its own rewards . Make sure to mention and that loan providers bring that one, and have every person lender regarding their unique words for upfront underwriting.

cuatro. What exactly is your average closing time?

An alternative vital matter. You’ll be amazed because of the version out-of closing minutes across the industry. As reported by Ellie Mae inside the , the average closure day is actually 43 weeks (the lowest it’s been because ). Make use of this shape since your baseline when comparing bank-to-lender, or lender-to-world. Also, be sure to ask the lender when they last determined their mediocre closing date. If their average are highest or lower than the industry standard, consider asking them as to the reasons. Preciselywhat are they performing more? Can there be a confident reason that the newest closure day are longer, basically is there a poor tradeoff to their faster closing go out?

5. What is your own customer happiness price?

Really loan providers proudly screen so it shape. When it is difficult to find, or if perhaps these include anxious to share its score, consider you to a red flag. In addition to query how they estimate its customer satisfaction get, and also the time it had been past computed. You dont want to feet the decisions off of old rates.